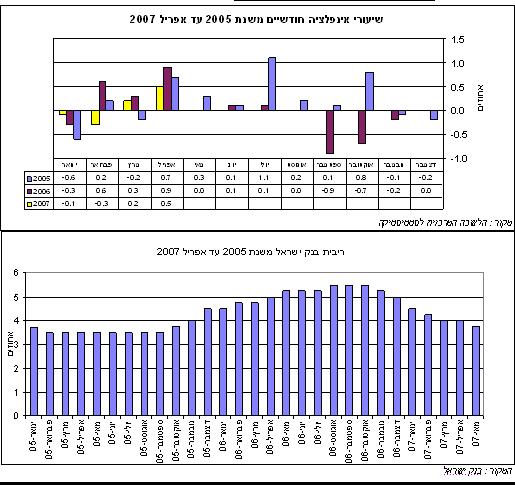

The predicted inflation for the entire year 2007 will amount to 0.7%, so don't get excited about the April index - 0.5%

The price index that rose by 0.5% in April was expected and reflects seasonal price increases (clothing and footwear, fruits and vegetables, etc.). Since the beginning of the year, the index has so far risen by 0.3%. We expect inflation in 2007 to amount to only 0.7%, which is below the lower limit of the 1% inflation target.

This forecast is mainly based on the assessment that the shekel, which has increased by a considerable rate of about 15% in the last fifteen months and reached NIS 3.93 per dollar, will continue to be strong. The chance, which we see, of a significant devaluation following the continuation of the Bank of Israel's policy is not high.

However, it is worth considering the possibility that the continued increase in the short-term interest rate gap between Israel and the US could also translate into a devaluation, perhaps sharp, when the catalyst could be the worsening of negative geopolitical processes, a fundamental crisis in the capital markets or a change in the tastes of foreign investors who contribute greatly Very much for the shekel.

The inflation derived from the capital market for 2007 is 0.5% and for the year ahead 0.5% as well, still below the lower limit of the inflation target. (This derivative inflation is calculated by the difference between non-linked and linked bond yields for the year). We expect inflation in the coming year inflation of 0.7%. Looking at the longer term, we expect that in 2008 inflation will amount to about 1.5%. The expected increase in inflation will reflect the cumulative effect of the lowering of the monetary interest rate, the accelerated economic growth and the decrease in unemployment.

Even in the expected inflationary profile and the path of further lowering of the interest rate, which we estimate will reach the level of 3.25%, we see an advantage in terms of risk/opportunity for capital gains specifically for medium-term corporate index-linked bonds and long-term government bonds over similar non-linked shekel bonds. We expect the yield to maturity in the long bonds to fall to about 2.75% (from the current level of about 2.95%). (This opinion should not be considered a recommendation or investment advice)

One response

Glad to see here also articles about finance (and not just Astro and Bio...)